Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Winsome Resources Limited - Case Study

Written: 12 August 2023

Winsome Resources (ASX:WR1) is a relatively new entrant to the ASX, having listed in late 2021 after raising $18m. The company's assets are a series of lithium claims in Canada, which were vended in by MetalsTech (ASX:MTC). This is a typical approach by companies with too many assets so separating out the businesses can create management focus and simplicity for investor mandates.

These unloved and undervalued assets can get a new breath of life in a newly listed vehicle, so examining the signs of future success can be very rewarding. Let's dive in to see if Winsome is in fact a "Triple Threat".

Threat 1: Setting goals

A company that is able to set goals and follow through with them is a great characteristic for investors. It creates predictability around the company's plans and how the management team expect go generate shareholder value. Through that, we can likely have a better sense on where our investment is headed in addition to the likely risks on that road.

Winsome has only been listed for less than 2 years at the time of writing, so has limited track record. However, if we examine the various market materials provided by management we can examine what tasks they have achieved, and if not, why not. After all, it's perfectly fine to adjust strategy but proper explanation should be provided to keep shareholders informed. Let's take a look.

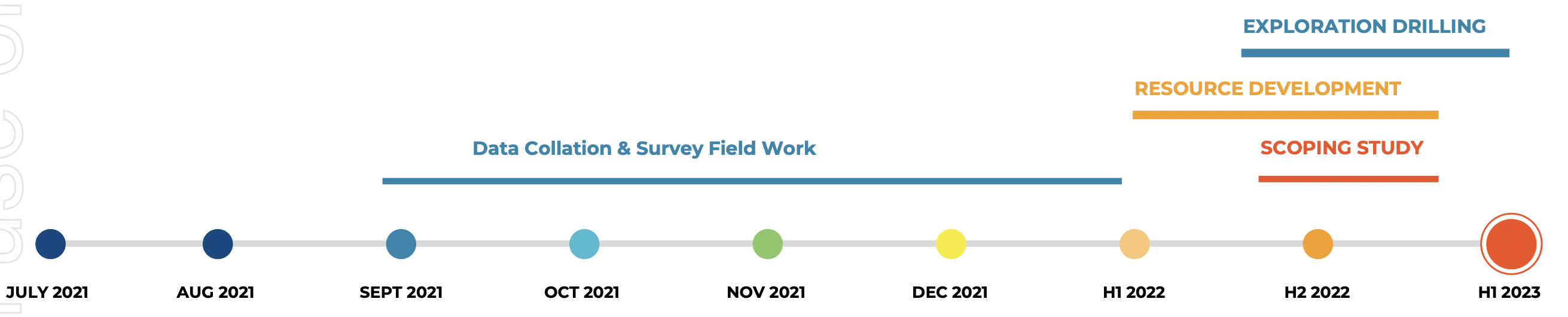

1 December 2022 Investor Presentation

Not long after the IPO, Winsome released an investor presentation (link) outlining the forward plan for the business. The company set out 3 goals so let's look at whether they've achieved their quoted timeline:

Winsome has only been listed for less than 2 years at the time of writing, so has limited track record. However, if we examine the various market materials provided by management we can examine what tasks they have achieved, and if not, why not. After all, it's perfectly fine to adjust strategy but proper explanation should be provided to keep shareholders informed. Let's take a look.

1 December 2022 Investor Presentation

Not long after the IPO, Winsome released an investor presentation (link) outlining the forward plan for the business. The company set out 3 goals so let's look at whether they've achieved their quoted timeline:

- Resource development: H1 2022 - H1 2023

- Exploration drilling: H2 2022 - H1 2023

- Scoping study: H2 2022 - H1 2023

If we examine the announcements following this, we can understand which of these goals they've achieved and within the timeline guided.

✅ Resource development - Infill drilling commenced Feb 2022. Link to the announcement.

✅ Exploration drilling - Drill test of new targets in the same program as above. Link to the announcement.

❌ Scoping study - delayed with no explanation given. The latest indication for the scoping study/PEA was “2023”

29 June 2022 Investor Presentation - link

✅ Resource development - Infill drilling commenced Feb 2022. Link to the announcement.

✅ Exploration drilling - Drill test of new targets in the same program as above. Link to the announcement.

❌ Scoping study - delayed with no explanation given. The latest indication for the scoping study/PEA was “2023”

29 June 2022 Investor Presentation - link

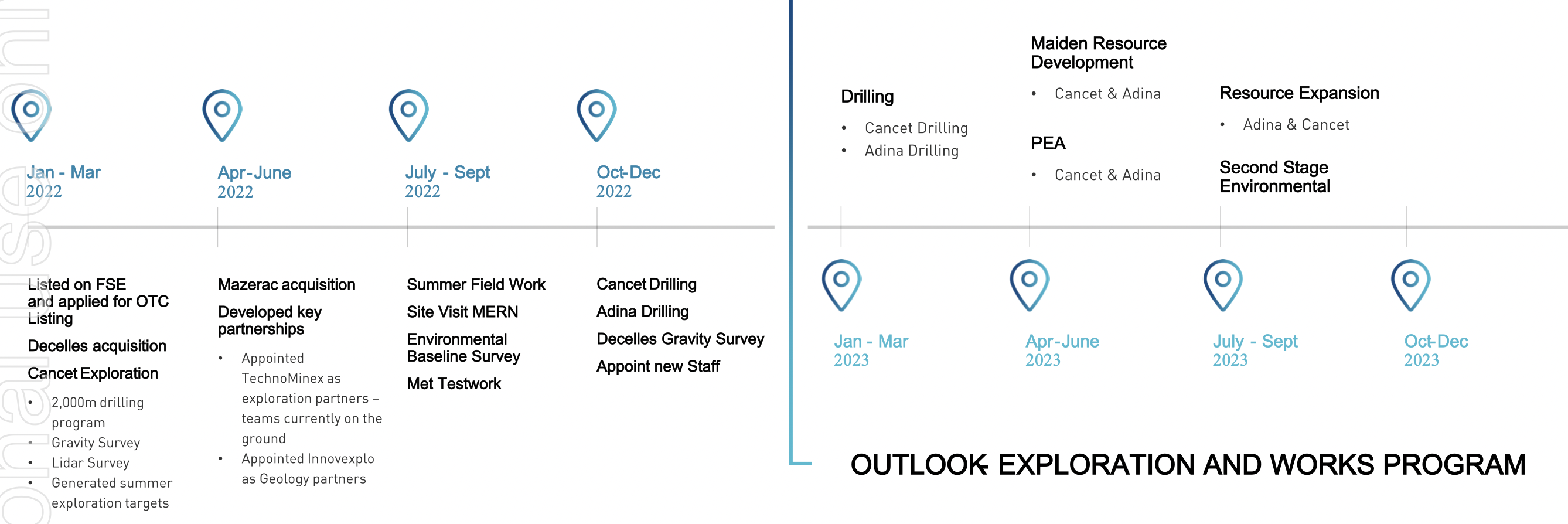

✅ Cancet Field Exploration - Surface stripping and dyke mapping commenced in August 2022. Link to the announcement.

✅ Cancet resource drilling - Drill mobilised commenced 14 October. Link to the announcement.

⚠️ Decelles & Mazerac field work - No word on Mazerac work but Decelles field work confirmed in 30 June quarterly. Link to the announcement.

✅ Adina field work - 3 week field trip completed on 16 August. Link to the announcement.

✅ Met test work - Already achieved at the time. No further evidence of met test work in H2. Link to the announcement.

4 November 2022 Investor Presentation - link

✅ Cancet resource drilling - Drill mobilised commenced 14 October. Link to the announcement.

⚠️ Decelles & Mazerac field work - No word on Mazerac work but Decelles field work confirmed in 30 June quarterly. Link to the announcement.

✅ Adina field work - 3 week field trip completed on 16 August. Link to the announcement.

✅ Met test work - Already achieved at the time. No further evidence of met test work in H2. Link to the announcement.

4 November 2022 Investor Presentation - link

✅ Adina Drilling - first round of assays received on 6 Jan in addition to an expansion of the drill program. Link to the announcement.

✅ Cancet Drilling - commencement of drilling mentioned in the 31 December 2022 announcement (link) but no material information provided in following announcements.

❌ Maiden Resource Development - no maiden resource announced in the timeframe and subsequently postponed to “2023”

❌ PEA - no PEA/scoping study announced in the timeframe and subsequently postponed to “2023”

❌ Resource Expansion - N/A given the maiden resource hasn't been announced yet.

▶️ Second Stage Environmental - TBCAs we can see below in the Jan 2023 investor presentation (link), the PEA, maiden resource and environmental study has been replaced with the generic term “study work”.

✅ Cancet Drilling - commencement of drilling mentioned in the 31 December 2022 announcement (link) but no material information provided in following announcements.

❌ Maiden Resource Development - no maiden resource announced in the timeframe and subsequently postponed to “2023”

❌ PEA - no PEA/scoping study announced in the timeframe and subsequently postponed to “2023”

❌ Resource Expansion - N/A given the maiden resource hasn't been announced yet.

▶️ Second Stage Environmental - TBCAs we can see below in the Jan 2023 investor presentation (link), the PEA, maiden resource and environmental study has been replaced with the generic term “study work”.

This is further affirmed in the April 2023 presentation (link) below.

As we can see, Winsome has broadly been punctual in keeping to their exploration guidance. Yet it is likely that they have reprioritised away from the maiden resource and PEA in favour of additional exploration; this small shift in strategy wasn't effectively communicated and often ignored in shareholder communications.

About setting goals

Threat 2: Equal capital raise access

The company has conducted two capital raises since listing on the ASX. Although this is a short track record, the company looks to be improving their shareholder equality during these corporate activities.

Raise 1: 15 November 2022

Winsome raised $6.8m via a placement, utilising the Canadian flow-through share provisions. The provisions can apply to certain Canadian critical mineral projects and offers generous tax incentives to Canadian investors who invest in such projects. For Winsome, the shares were placed to PearTree Securities Inc, a local Canadian firm, who is able to benefit from the tax provisions and in turn, allows Winsome to sell the shares at a higher price. The shares placed to PearTree is then block-traded to a local Australian broker for distribution to investors.

Due to the premium associated with the flow-through shares, Winsome raised at a 98% premium to the closing share price which then creates less dilution.

Unfortunately, no mechanism for shareholder participation in this case.

Raise 2: 3 February 2023

Winsome raised $50m which consisted of a $19m flow-through share placement and $31m share placement. This allowed the company to maximise the price received for the FTS component whilst also tapping additional demand via a standard placement.

Fortunately in this case, the company offered shareholders a generous $10m SPP. This allows existing shareholders to participate in the capital raise on the same term as external investors and is a great move by management to ensure an equal playing field.

About equal capital raise access

Raise 1: 15 November 2022

Winsome raised $6.8m via a placement, utilising the Canadian flow-through share provisions. The provisions can apply to certain Canadian critical mineral projects and offers generous tax incentives to Canadian investors who invest in such projects. For Winsome, the shares were placed to PearTree Securities Inc, a local Canadian firm, who is able to benefit from the tax provisions and in turn, allows Winsome to sell the shares at a higher price. The shares placed to PearTree is then block-traded to a local Australian broker for distribution to investors.

Due to the premium associated with the flow-through shares, Winsome raised at a 98% premium to the closing share price which then creates less dilution.

Unfortunately, no mechanism for shareholder participation in this case.

Raise 2: 3 February 2023

Winsome raised $50m which consisted of a $19m flow-through share placement and $31m share placement. This allowed the company to maximise the price received for the FTS component whilst also tapping additional demand via a standard placement.

Fortunately in this case, the company offered shareholders a generous $10m SPP. This allows existing shareholders to participate in the capital raise on the same term as external investors and is a great move by management to ensure an equal playing field.

Threat 3: Spending to grow

Using capital effectively is very strong quality and shows that the company is maximising growth with shareholder funds.

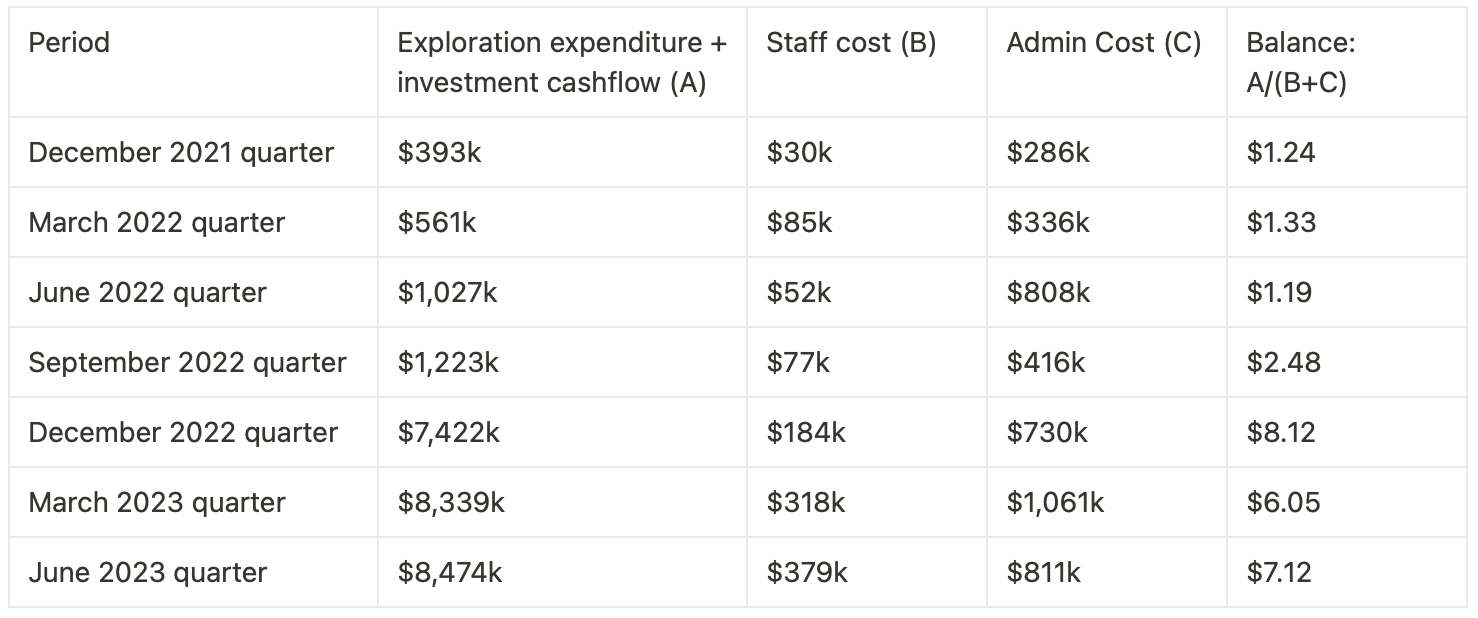

For Winsome, it looks like the company spent the first few quarters post-IPO setting up the foundations and structuring the forward growth plan. This can be seen during this period of relatively quiet activity and less capital intensive work. If we look at the ratio between exploration expenditure + investment cash outflow vs staff + admin cost, we can see a similar story:

For Winsome, it looks like the company spent the first few quarters post-IPO setting up the foundations and structuring the forward growth plan. This can be seen during this period of relatively quiet activity and less capital intensive work. If we look at the ratio between exploration expenditure + investment cash outflow vs staff + admin cost, we can see a similar story:

The figure we are interested in here is the final column, which looks at the ratio of the investment “growth” activities relative to administration and people cost. Usually, a figure above $3.5 is a good benchmark and shows that the company is efficiently using capital and not overpaying for the people used to execute the work program.

Understandably for Winsome, the 4 quarter period after an IPO shows below-optimal capital efficiency. Fortunately, the ratio drastically improves in the following quarters as the ground work laid out previously pays off. This is a very strong ratio that the management team have been able to deliver and hopefully they are able to maintain this level of optimisation as the company develops.

About spending to grow

Understandably for Winsome, the 4 quarter period after an IPO shows below-optimal capital efficiency. Fortunately, the ratio drastically improves in the following quarters as the ground work laid out previously pays off. This is a very strong ratio that the management team have been able to deliver and hopefully they are able to maintain this level of optimisation as the company develops.

My concluding thoughts

Winsome is showing all the right indications of a well run company that has a decent chance of growing into a successful business in the medium term. The company has largely followed up on their promises and clearly have a deep respect for shareholder capital. As such, they are likely to continue governing in the spirit of directorship.

Additional areas of improvement can be sought in transparency and communication - even if priorities alter and goals adapt, it is better to be upfront on this rather than ignoring it altogether. When explained well, shareholders embrace change.

Nevertheless, we see Winsome Resources as a rare Triple Threat.

Winsome is showing all the right indications of a well run company that has a decent chance of growing into a successful business in the medium term. The company has largely followed up on their promises and clearly have a deep respect for shareholder capital. As such, they are likely to continue governing in the spirit of directorship.

Additional areas of improvement can be sought in transparency and communication - even if priorities alter and goals adapt, it is better to be upfront on this rather than ignoring it altogether. When explained well, shareholders embrace change.

Nevertheless, we see Winsome Resources as a rare Triple Threat.

Register for the next Triple Threat update

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.